Are you a real estate investor struggling to qualify for traditional financing? Whether you’re self-employed, have multiple rental properties, or simply want to leverage your property’s income potential rather than your personal finances, DSCR loan qualifications offer a game-changing solution. These specialized investment property loans have revolutionized how real estate investors access capital, and understanding the qualification requirements is your first step toward expanding your portfolio.

Key Takeaways:

- DSCR loan qualifications focus on property cash flow rather than personal income

- Minimum credit scores typically range from 620-680, with better terms at 700+

- Down payments start at 20% for most properties, with some lenders offering 15% for excellent credit

- The debt service coverage ratio should ideally be 1.25 or higher for best terms

- No income verification required – perfect for self-employed real estate investors

What Makes DSCR Loan Qualifications Different?

A DSCR loan is a type of mortgage for an investment property where the lender qualifies the borrower based on the expected rental income of the property rather than traditional income documentation like tax returns or W-2s. This fundamental shift in how lenders evaluate borrowers has opened doors for many real estate investors who previously struggled with conventional loan requirements.

The magic behind these qualifications lies in the debt service coverage ratio itself. The DSCR includes a property’s annual net operating income and mortgage debt (principal and interest). It’s used to gauge cash flow from a property and how much of the income can be allocated towards the monthly loan payment.

For example, if a property generates $3,000 monthly in rental income and has total monthly debt obligations of $2,400, the DSCR would be 1.25 ($3,000 ÷ $2,400). This means the property generates 25% more income than needed to cover its debt payments – exactly what lenders want to see.

Essential DSCR Loan Requirements: The Four Pillars

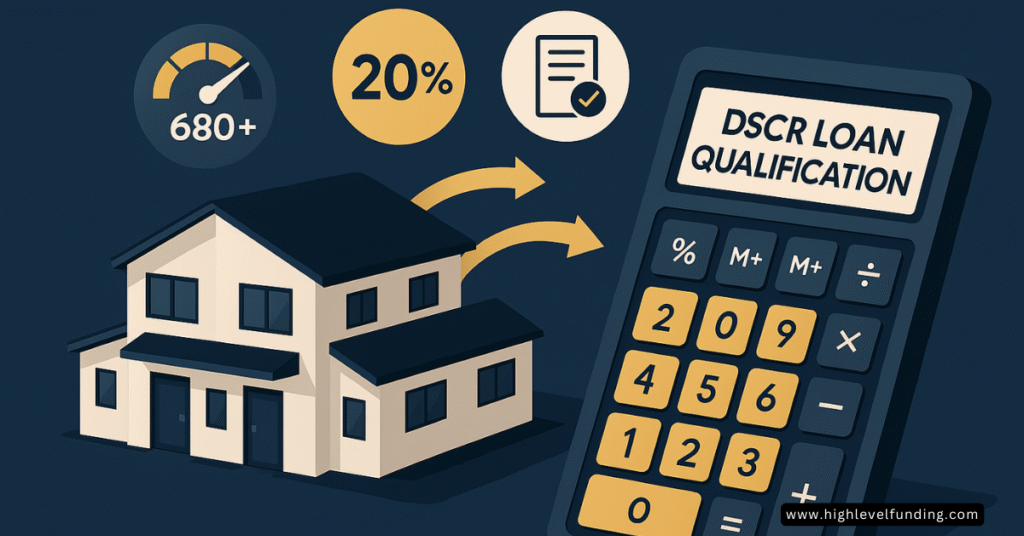

1. Credit Score Requirements: Your Financial Foundation

Most lenders require a minimum FICO score of 660 to qualify for a DSCR loan, though this threshold can vary depending on the loan-to-value ratio. However, I’ve found that credit score requirements have become more nuanced in 2025:

- Minimum threshold: 620-640 for most lenders

- Preferred range: 680-700 for standard terms

- Premium terms: 740+ for the best interest rates and lowest down payments

For investors with excellent credit, some lenders offer DSCR loans with only 15% down (85% LTV) for loan amounts up to $1 million when you have a 740+ credit score. This represents a significant advantage for high-credit borrowers.

What’s particularly interesting is that some specialized lenders will work with credit scores as low as 550, though this comes with stricter terms and higher down payment requirements.

2. Down Payment and Loan-to-Value Requirements

The down payment landscape for DSCR loans has evolved considerably. Here’s what you need to know:

Standard Requirements:

- Single-family homes: 20% minimum down payment

- Multi-family properties (2-4 units): 25% minimum down payment

- Commercial properties: Often 30% or higher

The down payment requirement for a DSCR loan generally hinges on the loan-to-value (LTV) ratio offered by the lender. In most cases, investors can expect to provide a down payment ranging from 20% to 25% of the property’s purchase price.

Factors That Influence Down Payment Requirements:

- Your credit score and financial profile

- The property’s DSCR ratio

- Property type and condition

- Loan amount and term

- Regional market conditions

3. The DSCR Ratio: Your Property’s Report Card

The debt service coverage ratio is the heart of your qualification. A minimum DSCR of 1.00 is generally accepted by lenders, meaning the property brings in enough rental income to cover its monthly debt payments. However, a DSCR of 1.25 or higher is preferred, as it indicates a healthy cushion and often leads to better loan terms.

DSCR Benchmarks:

- 1.0: Break-even (acceptable but may require higher down payment)

- 1.1-1.24: Good (standard terms)

- 1.25+: Excellent (best rates and terms)

- Below 1.0: Possible with specialized “No Ratio” programs

Here’s how different DSCR ratios affect your loan terms:

| DSCR Ratio | Down Payment | Reserves Required | Interest Rate Impact |

|---|---|---|---|

| 1.25+ | 20-25% | 3-6 months | Best rates |

| 1.0-1.24 | 20-25% | 6 months | Standard rates |

| 0.75-0.99 | 25-30% | 6-12 months | Higher rates |

4. Cash Reserves: Your Safety Net

Most lenders will require you to have three to six months of reserves in a savings account in case you run into vacancy issues or other problems. The exact amount depends on:

- Your DSCR ratio (lower ratios require more reserves)

- Number of properties in your portfolio

- Property type and location

- Your experience as a landlord

Property Requirements: What Qualifies for DSCR Financing

Not all properties are created equal in the eyes of DSCR lenders. Eligible properties include single-family homes, duplexes, multi-family properties (up to 4 units), and some mixed-use properties on a case-by-case basis.

Eligible Property Types:

- Single-family rental homes

- Duplexes, triplexes, and fourplexes

- Condominiums and townhomes

- Small multi-family buildings

- Some mixed-use properties

- Short-term rental properties (Airbnb/VRBO)

Property Condition Requirements: Most lenders require properties to be in “turnkey” condition – ready to rent without major repairs. Turnkey means the property doesn’t require any renovation; you can “turn the key and go.”

The DSCR Loan Application Process: A Step-by-Step Walkthrough

Unlike conventional loans, the DSCR loan process is streamlined but requires different documentation:

Step 1: Initial Qualification and Pre-Approval

Your lender will review your basic qualifications:

- Credit score verification

- Down payment confirmation

- Property details and intended use

Step 2: Property Analysis and Appraisal

An appraisal that includes a market rent schedule (typically Form 1007) is required to substantiate the income. This is crucial because the appraiser will:

- Determine fair market value

- Analyze comparable rental properties

- Establish market rent potential

- Calculate the DSCR ratio

Step 3: Documentation Submission

DSCR loans have lighter documentation requirements than conventional loans, requiring only what is necessary and reasonable to qualify for the loan.

Required Documents:

- Loan application

- Credit authorization

- Property purchase agreement or current deed

- Bank statements (2-3 months)

- LLC formation documents (if applicable)

- Property insurance information

NOT Required:

- Tax returns

- W-2 forms or pay stubs

- Employment verification

- Personal income documentation

Step 4: Underwriting and Approval

The underwriter focuses primarily on:

- Property cash flow analysis

- Credit history review

- Asset verification

- Property condition assessment

Step 5: Closing

DSCR loans typically close quicker than others, based on the fact that there is little to no personal financial information required. Most close within 3-5 weeks from application.

| Related: DSCR vs Traditional Loan Comparison

Advanced Qualification Strategies

Maximizing Your DSCR Ratio

If your property’s DSCR is borderline, consider these strategies:

- Choose longer loan terms: Opting for a 40-year term instead of 30 years reduces monthly payments

- Interest-only options: Some lenders offer interest-only periods to improve cash flow

- Property improvements: Strategic renovations can justify higher rental income

Entity Structure Considerations

You may close in the name of your LLC, Corporation, LLP, LLLP, or other entity. This is a popular option for tax savings purposes, as well as limiting personal liability exposure.

Benefits of Using an Entity:

- Personal liability protection

- Potential tax advantages

- Professional appearance to tenants

- Easier portfolio management

Working with Specialized Lenders

Not all lenders are created equal in the DSCR space. Look for lenders who:

- Specialize in investment property financing

- Offer competitive rates and terms

- Have experience with your property type

- Provide clear communication throughout the process

DSCR Loan Qualifications – Common Qualification Challenges and Solutions

Challenge 1: Properties Without Rental History

Solution: For properties not meeting standard DSCR requirements, consider specialized “No RATIO PRO” programs that bypass the need for income or cash flow verification entirely.

Challenge 2: Credit Score Below 680

Solution:

- Work on improving your credit score before applying

- Consider lenders who specialize in lower credit scores

- Increase your down payment to offset credit risk

- Provide additional cash reserves

Challenge 3: Complex Property Types

Solution:

- Work with lenders experienced in your property type

- Provide detailed rental market analysis

- Consider alternative documentation for income verification

2025 Market Updates and Trends

The DSCR loan market continues to evolve. In 2025, lenders have taken steps to clarify and improve DSCR loan offerings with clearly defined minimum DSCR thresholds and streamlined appraisal requirements.

Key 2025 Updates:

- More lenders entering the market (increased competition)

- Clearer qualification guidelines

- Improved rate competitiveness

- Expanded property type acceptance

- Better terms for experienced investors

Is a DSCR Loan Right for You?

DSCR loans are ideal for:

- Self-employed real estate investors

- Investors with multiple properties

- Foreign nationals investing in US real estate

- Anyone whose tax returns don’t reflect true income capacity

- Investors focused on cash flow properties

They may not be suitable if:

- You need owner-occupied financing

- You have limited capital for down payments

- You’re looking for the absolute lowest interest rate

- The property has poor income potential

Taking Action: Your Next Steps

Understanding DSCR loan qualifications is just the beginning. To move forward:

- Assess your current situation against the qualification requirements outlined above

- Identify potential properties that meet the income requirements

- Connect with specialized DSCR lenders to compare terms and requirements

- Prepare your documentation and financial information

- Consider working with an experienced agent who understands investment properties

The world of real estate investing continues to evolve, and DSCR loans represent one of the most powerful tools available to today’s investors. By understanding these qualification requirements and preparing accordingly, you’re positioning yourself to take advantage of opportunities that others might miss.

Whether you’re acquiring your first rental property or expanding an existing portfolio, DSCR loan qualifications offer a flexible path to financing that aligns with the realities of modern real estate investing. The key is preparation, understanding, and working with the right lending partners who appreciate the unique needs of today’s real estate investors.

Ready to explore DSCR financing for your next investment? Start by getting pre-qualified with a specialized lender to understand exactly what you qualify for based on your specific situation and investment goals.

Frequently Asked Questions

Q: Can I qualify for multiple DSCR loans simultaneously?

A: There is no limit to the number of DSCR loans you can qualify for. This means that investors who own multiple real estate properties can take out multiple loans to generate income from many tenants.

Q: Do I need real estate investment experience?

A: While not always required, having previous landlord experience can strengthen your application and potentially improve your terms.

Q: Can I use a DSCR loan for a primary residence?

A: No, DSCR loans are strictly for investment properties. You cannot live in a property financed with a DSCR loan.

Q: How long does the approval process take? A: Most DSCR loans close within 3-5 weeks, faster than conventional mortgages due to reduced documentation requirements.

Q: Can I refinance an existing property with a DSCR loan?

A: Yes, DSCR loans can be used for both purchases and refinances, including cash-out refinances up to 75% LTV.